Parents play a vital role in shaping a child’s financial future. Introducing money concepts early fosters confidence and responsibility. This guide offers age-tailored strategies, psychological insights, and practical activities to turn everyday moments into powerful learning opportunities.

Financial literacy is more than math—it’s about decision making, planning, and self-reliance. Research shows that early exposure reverses negative cycles and drastically reduces adult debt and stress.

Without formal instruction, many young adults struggle with credit cards, budgets, and unplanned expenses. By stepping in, parents can provide clear guidance based on proven principles and nurture a mindset of wise money choices.

Children’s cognitive and emotional abilities evolve rapidly. Tailoring lessons to each stage ensures concepts stick and enthusiasm stays high. Below, discover core themes and recommended activities from preschool through the teen years.

At this stage, kids begin to recognize coins and bills and link money to objects they want. Simple games and playful experiments lay the groundwork for future budgeting and sharing skills.

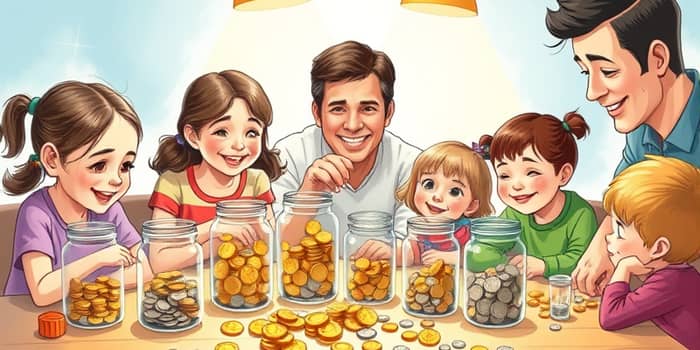

Activities might include sorting real coins by size and color, or using transparent containers for a visual representation of savings growth. Pretend stores with toy money encourage role play and basic counting.

Children can now count money, make change, and understand cause and effect. They delight in setting concrete goals—saving for a toy, for example—and watching progress each week.

Introduce an allowance system that connects chores to earnings. A three-jar method with save, spend, and share jars encourages balanced decision making and empathy when a portion goes to charity.

Tweens grasp the relationships between income and expenses. They enjoy challenges like planning a small business or tracking a pretend investment portfolio.

Encourage projects such as bake sales or pet-sitting. Digital budgeting apps can reinforce lessons and demonstrate connecting effort directly to income. Invite tweens to help compare prices online and research best deals.

Teens are ready for real banking, debit cards, and the basics of credit. They can manage sub-accounts, set up direct deposits, and learn about taxes and insurance.

Offer supervised experiences: let them cover a small bill, monitor fee statements, and practice responsible card use. Discuss long-term goals like college or a car to build long-term planning skills.

These tools make abstract ideas concrete and fun. Involving kids in real decisions transforms chores into learning opportunities and fosters active participation in household finances.

Children learn best by example. When parents discuss budgets, open account statements, or compare insurance plans, kids absorb both practical skills and mindsets.

Spontaneous teachable moments—like withdrawing cash from an ATM or reviewing a grocery receipt—reinforce classroom concepts with real-world impact. A routine family finance meeting normalizes money conversations.

Parents may hold different philosophies on spending or saving. Presenting a united front around core values—such as generosity, wise planning, and avoiding debt—builds consistency.

Reconcile differences privately to prevent confusion. Highlight that responsible money habits are universal, even if approaches vary. Sharing family financial goals fosters cohesion.

Guidelines often suggest a child’s allowance equals one dollar per week per year of age. Savings goals of 10 to 40 percent of income encourage discipline. Surveys show kids with parental guidance score significantly higher on financial tests.

Starting lessons as early as age three has been linked to improved money confidence in adulthood and a lasting appreciation for planning.

Awareness of these pitfalls allows parents to intervene early, turning mistakes into valuable lessons rather than setbacks.

By integrating these principles into daily life, parents lay a foundation for lifelong financial health. Each age stage builds on the last, guiding children toward adulthood with confidence and competence.

References